What happens to the money in your retirement plan account when you switch jobs? That’s up to you. Typically, one of your options may be to take your savings in a single sum. Sounds like a bonus, right? Wrong. Learn about why you should put more thought into cashing out your retirement savings.

Early 401(k) Withdrawals May Result in More Taxes and Penalties

Before you drain your account, make sure you understand how a cash-out works, because you may be in for some surprises.

The first surprise is that you won’t get to keep the full amount. Since the money in your retirement savings account generally has not been taxed, you’ll have to include the distribution as income on your federal (and possibly state) income tax return. Additional income means you’ll owe additional income tax. The retirement plan is required to withhold 20% to send to the IRS as a “down payment” on your overall federal income tax liability for the year.

Another surprise – you may also owe a 10% early withdrawal penalty. In the end, your tax liability could be anywhere from 20-30+% of your retirement account balance.

Distributions Now Mean Less Money Later

Not only will you get less money when you cash out, but taking a distribution and not reinvesting the money for retirement could also mean ending up with less in the future. One reason is that you would miss out on compounding interest over the year. Even if it’s still early in your career, taking a distribution, paying the taxes and any penalty that applies, and spending what’s left could make it harder to reach your retirement savings goals.

How You Can Keep Your Retirement Savings Growing

Instead of cashing out, consider keeping your savings in a tax-deferred account. Here are the possible options:

- Leave your savings in your old employer’s plan (if permitted)

- Roll over your money into your new employer’s plan (assuming rollovers are accepted)

- Roll over your money into an individual retirement account (IRA)

While there are always special circumstances when it comes to taking your savings in a single sum, the long-term benefits of staying in a tax-deferred account will have a meaningful impact when you retire.

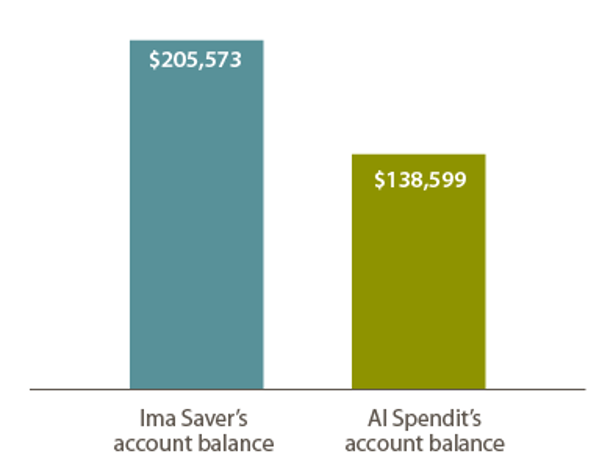

Example Retirement Savings Scenario

Ima Saver and her friend Al Spendit both had $15,000 in their retirement accounts when they changed jobs. Ima rolled over her balance into her new employer’s plan and contributed $200 a month for the next 25 years. Al cashed out and started over. He also joined his new employer’s plan and, like Ima, contributed $200 a month for 25 years. However, his balance never caught up. Even though they contributed the same amount and had identical earnings, Ima’s account balance is significantly more than Al’s because she kept her savings going.

This hypothetical example is for illustrative purposes only. It assumes a monthly contribution of $200 and an average annual return of 6% (compounded monthly). It does not represent any specific investment product offered by your plan and does not include any investment fees and expenses. Your investment returns will differ, and it is unlikely that your contribution amount will remain the same over a long period. Pre-tax contributions and related plan earnings will be subject to ordinary income taxes and a possible early withdrawal penalty upon distribution.

Get Professional Insights

When you change jobs, you have enough on your mind. Reaching out to a financial professional, like a member of the Emerj360 team, can help clear up any confusion you may have by simply having a conversation to discuss your options. You’ve worked hard for the retirement funds you’ve saved so far. Keep them working for you!